Your 2025 Guide to Buying a Home in Merritt: Incentives, Taxes and Market Insights for First-Time Buyers

With its friendly pace, beautiful Nicola Valley surroundings, and more accessible price tags than BC’s bigger cities, Merritt is quickly becoming a smart choice for new homeowners. Whether you’re just starting to save or already pre-approved for a mortgage, understanding your options can save you thousands, and help you feel more confident every step of the way.

This guide breaks down what you need to know as a first-time home buyer in Merritt in 2025, including local market trends, BC and federal incentives, new tax rules, and a simple step-by-step to buying your first place.

Let’s start with the big question: Why Merritt?

Why Merritt Makes Sense for First-Time Buyers

Buying your first home is a big decision, and where you buy matters just as much as what you buy. Merritt checks a lot of boxes for first-time buyers looking for value, lifestyle, and long-term potential.

Here’s why Merritt stands out in 2025:

- Affordable compared to BC’s larger markets. With average home prices well below those in Kelowna or Vancouver, Merritt offers first-time buyers a chance to get into the market without overstretching.

- A close-knit, outdoor-loving community. From hiking in the hills to summers on Nicola Lake, Merritt’s active lifestyle appeals to younger buyers and families alike.

- Proximity to major hubs. Just under two hours to Kelowna and Kamloops, Merritt offers quiet, small-town living without losing access to larger city amenities.

Plus, many provincial and federal first-time buyer programs are available here, just as they are in BC’s bigger centres—but they stretch further in a more affordable market like Merritt.

Merritt’s Real Estate Market in 2025

Understanding the local housing market is key when you're deciding where—and when—to buy your first home. Merritt offers first-time buyers a rare combination: relative affordability, less competition, and the breathing room to make thoughtful decisions.

Let’s take a closer look at the current landscape.

Home Prices, Inventory & Buyer Conditions

As of mid-2025, Merritt’s average home price sits around $435,000, a modest year-over-year increase of 3.2%. This pace reflects a balanced market—one that favours neither buyers nor sellers too aggressively.

What this means for you:

- Detached homes and townhomes remain within reach for buyers putting down 5% to 10%.

- Inventory is stable, with more homes available than during the high-demand years of 2021–2022.

- Fewer bidding wars, especially compared to urban BC markets.

Many local agents are seeing more first-time buyers in Merritt now than ever before, especially those priced out of Kelowna and the Lower Mainland.

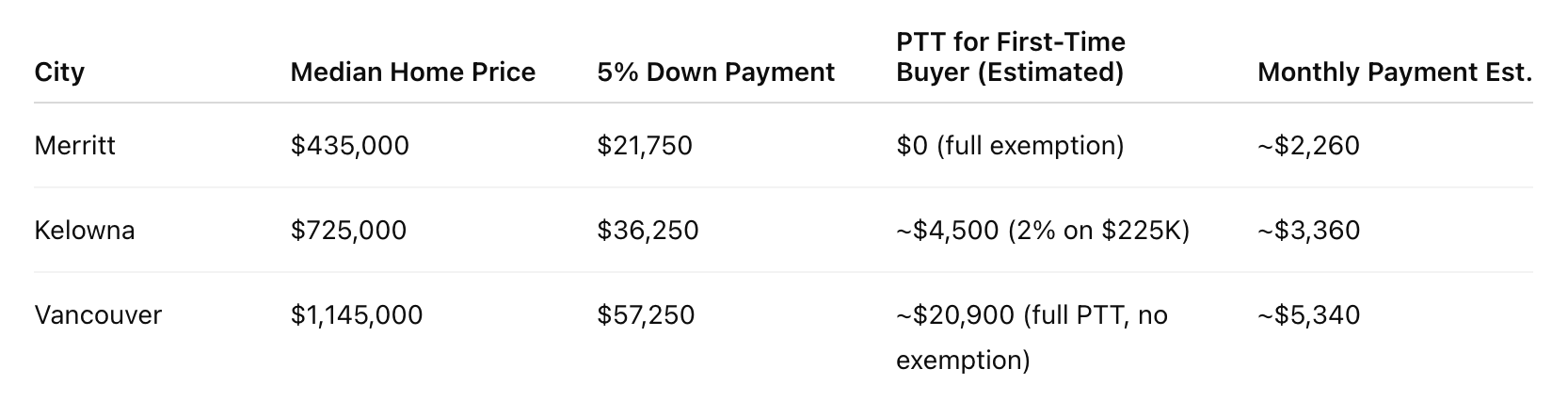

Merritt vs. Larger BC Cities

Let’s compare what it actually costs to buy a starter home in Merritt versus Kelowna and Vancouver.

Merritt vs Kelowna vs Vancouver – First-Time Buyer Snapshot (2025)

As the table shows, Merritt offers a much softer financial entry point—especially when it comes to the Property Transfer Tax (PTT), which we’ll break down next.

BC Incentives for First-Time Buyers

If you’re a first-time home buyer, there are three major BC programs that could reduce your upfront costs or help with affordability after you move in. These incentives apply whether you’re buying in a big city or a smaller market like Merritt—but they go further when home prices are lower.

Let’s break them down one by one.

Property Transfer Tax Exemption

The Property Transfer Tax (PTT) is a provincial tax due when you buy real estate in BC. It’s normally:

- 1% on the first $200,000

- 2% on the portion between $200,000 and $2 million

But if you're a first-time buyer and your home is priced under $835,000, you qualify for a full exemption.

That means:

- No PTT to pay (a savings of up to $8,000)

- Applies to resale or new homes

- You must plan to live in the home as your principal residence

If your purchase price falls between $835,000 and $860,000, you may still qualify for a partial exemption.

Newly Built Home Exemption

Buying a brand-new home or pre-sale condo in Merritt?

You could qualify for the Newly Built Home Exemption, which eliminates the PTT on homes up to $1,100,000 (new threshold as of April 2024).

Key requirements:

- The home must be newly constructed and never lived in

- You must move in within 92 days and use it as your principal residence

- Applies to both detached homes and strata units

Even homes between $1,100,000 and $1,150,000 may be eligible for a partial exemption.

Home Owner Grant

Once you’ve moved in, the Home Owner Grant (HOG) can help reduce your annual property taxes.

In Merritt, you likely qualify for the regular grant of up to $770, if:

- Your home’s assessed value is under $2.15 million

- You live in the home as your primary residence

- You apply each year through the BC government portal

Bonus: Seniors, veterans, and people with disabilities may be eligible for additional savings under the HOG program.

These provincial programs can shave thousands off your total costs—especially valuable when every dollar counts in your first purchase.

New Taxes & What They Mean

2025 brought in some key tax updates that every BC home buyer should know about—even if you're not planning to sell anytime soon. While most of these new measures are aimed at short-term investors and flippers, it's still important to understand how they work (and whether they apply to you).

The 2025 BC Home-Flipping Tax

Introduced on January 1, 2025, the BC Home-Flipping Tax is designed to discourage quick resales of property that drive up prices.

Here’s what it means:

- If you sell a property within 2 years of buying it, you could be taxed up to 20% on the profit.

- The tax is highest (20%) if you sell within the first year, and decreases gradually until the two-year mark.

- Applies to all property types—including condos, townhomes, and detached houses.

- It’s in addition to federal and provincial income taxes.

Exemptions exist for life events like divorce, job relocation, death, or illness.

Other Taxes to Be Aware Of

Here are a few more taxes you might hear about when buying a home in BC:

- Speculation and Vacancy Tax (SVT):

Doesn’t apply in Merritt as of 2025. This tax targets homes left vacant in urban centres like Kelowna and Vancouver. - Foreign Buyer Ban (Federal):

Still in effect for 2025. If you're not a Canadian citizen or permanent resident, you cannot purchase residential property in most parts of Canada—including Merritt. - GST on New Homes:

If you're buying a new build, you’ll typically pay 5% GST on the purchase price.

The good news? There’s a GST New Housing Rebate—we’ll cover that in the next section.

So while none of these taxes should stop you from buying, understanding them helps you plan smarter, especially if you’re eyeing a brand-new build or planning a move before two years are up.

Federal Incentives You Can Use

In addition to BC’s provincial programs, the federal government offers several tools to support first-time buyers across Canada. These programs can help you boost your down payment, reduce your taxes, and make buying more manageable.

Let’s walk through your main options.

First Home Savings Account (FHSA)

The First Home Savings Account (FHSA) is one of the most powerful tools available to Canadian first-time buyers right now.

Here’s how it works:

- You can contribute up to $8,000 per year, to a lifetime maximum of $40,000.

- Contributions are tax-deductible—just like an RRSP.

- Withdrawals for a qualifying home purchase are completely tax-free—like a TFSA.

- Funds must be used to buy your first home within 15 years of opening the account.

If you’re buying in 2025 and have an FHSA in place, your savings could give you a significant boost toward your down payment.

💡 You can combine your FHSA with the RRSP-based Home Buyers’ Plan—doubling your tax-advantaged savings potential.

Home Buyers’ Plan (RRSP)

The Home Buyers’ Plan (HBP) allows you to withdraw money from your Registered Retirement Savings Plan (RRSP) to help fund your first home.

Key points:

- You can withdraw up to $60,000 (increased from $35,000 in 2024).

- The withdrawal is tax-free, as long as you repay it over 15 years.

- You must be a first-time buyer, and the home must be your principal residence.

You don’t have to choose between the HBP and the FHSA—you can use both if you’re eligible.

Home Buyers’ Tax Credit & GST/HST Rebate

There are two more federal programs worth knowing about:

- Home Buyers’ Tax Credit (HBTC):

A $10,000 non-refundable tax credit that can reduce your income tax owing by up to $1,500 in the year you buy your home. - GST/HST New Housing Rebate:

If you’re buying a newly built home, you may qualify for a partial GST rebate, depending on the home’s price and your eligibility.

In BC, the full rebate applies to homes priced $350,000 or less, with a partial rebate available up to $450,000.

While Merritt’s prices are higher than $350K, some smaller new builds and modular homes may still qualify.

What the Future Looks Like for Merritt Buyers

Here’s what the road ahead looks like:

- Moderate price growth is expected. Analysts project Merritt’s home prices will continue to rise slowly—about 2–4% annually over the next few years. That’s a healthy pace that supports long-term value without putting new buyers in a pressure cooker.

- Infrastructure investments are increasing. Projects like road upgrades, school expansion, and improved medical services are already underway—signs that Merritt is preparing for responsible growth.

- More buyers are arriving from larger cities. With Kelowna and Vancouver becoming increasingly out of reach, more young families and remote workers are relocating to smaller centres like Merritt, fueling local demand.

What does this mean for you?

✔️ You’re likely buying into a community on the rise, where your investment can grow

✔️ You’ll still find space, pace, and affordability that’s hard to match elsewhere in BC

✔️ Merritt is building for the future—with you in mind

Step-by-Step: Buying a First Home in Merritt

Buying your first home can feel overwhelming—but it doesn’t have to be. Whether you’re weeks away from making an offer or just starting to browse listings, having a roadmap helps everything feel more manageable.

Here’s a clear breakdown of what to expect as a first-time buyer in Merritt:

10 Steps to Buying a First Home in Merritt (2025)

[ ] 1. Get pre-approved for a mortgage

[ ] 2. Open an FHSA or RRSP (or both) and maximize savings

[ ] 3. Research Merritt neighbourhoods and housing types

[ ] 4. Connect with a local real estate agent (hi 👋)

[ ] 5. Estimate your total budget, including closing costs and taxes

[ ] 6. View homes in your price range and attend open houses

[ ] 7. Make an offer and negotiate terms

[ ] 8. Hire a home inspector and finalize financing

[ ] 9. Complete legal paperwork and pay your deposit

[ ] 10. Take possession and move in!

A few extra tips:

- Start with the math. Your pre-approval and down payment size will shape what’s realistic—and prevent heartbreak.

- Ask questions at every stage. There are no dumb questions. A good agent will walk you through everything patiently.

- Plan for move-in costs. Set aside extra for things like utilities, furniture, or small repairs in the first few months.

First-Time Buyer FAQs

1. Do I qualify as a first-time home buyer in BC?

Yes, if you’ve never owned a home anywhere in the world, or haven’t owned and lived in a home for at least four years, you likely qualify. Most BC and federal programs define “first-time buyer” the same way.

2. How much do I need for a down payment in Merritt?

The minimum down payment is:

- 5% for homes under $500,000

- 5% on the first $500,000, plus 10% on any amount above that, for homes up to $999,999

On a $435,000 home in Merritt, that’s a minimum down payment of $21,750.

3. Can I use both an FHSA and RRSP to buy my first home?

Yes! You can combine the First Home Savings Account with the Home Buyers’ Plan (RRSP) to maximize your down payment using tax-free or tax-deferred funds.

4. Is buying in Merritt better than renting?

In many cases, yes—especially with programs like the Property Transfer Tax exemption and stable home prices. If you plan to stay for at least 3–5 years, buying can be more cost-effective in the long run.

5. Do I pay GST when I buy a home?

- No GST on most resale homes

- Yes, 5% GST on new construction—but you may qualify for the GST New Housing Rebate if the home is under $450,000

6. What closing costs should I plan for?

Besides your down payment, budget for:

- Legal fees ($1,200–$1,800)

- Home inspection ($400–$600)

- Property appraisal (if required)

- Moving expenses

- Utilities setup

If you qualify for PTT exemptions, your closing costs will be significantly lower than in larger BC markets.

Conclusion & Next Steps

You’ve now seen how Merritt stacks up in the Nicola Valley housing market, how BC and federal programs can save you thousands, and what the actual steps to buying your first home look like. Whether you’re just starting to save or already house hunting, you’re ahead of the curve by getting informed and thinking long-term.

Thinking about taking the next step? I’d love to help you navigate your first home purchase—from finding the right property to understanding your financing and tax-saving options.

Let’s talk about what’s possible in 2025. Whether you want to explore available homes or just ask a few questions over coffee, I’m here for you.